As anyone involved in the consumer product space can attest, it’s a different ballgame than it was just a short time ago. In the U.S. for example, the largest food and beverage manufacturers have lost about $2 billion in market share to smaller operators. So while it’s been well documented in the first half of 2017 that smaller companies are pulling ahead of the pack and driving much of the growth in the U.S. fast-moving consumer goods (FMCG) realm, the trend begs the question: Is size the new determining factor for success, or can large companies advance too?

To find out what levers smaller brands are pulling to move the needle, Ravi Dhar, a professor of management and marketing at the Yale School of Management, sat down with the leaders of two very different medium-sized companies at Nielsen’s recent CoNEXTions event to find out how they’re gaining share and growing their businesses amid very challenging times for the U.S. retail market.

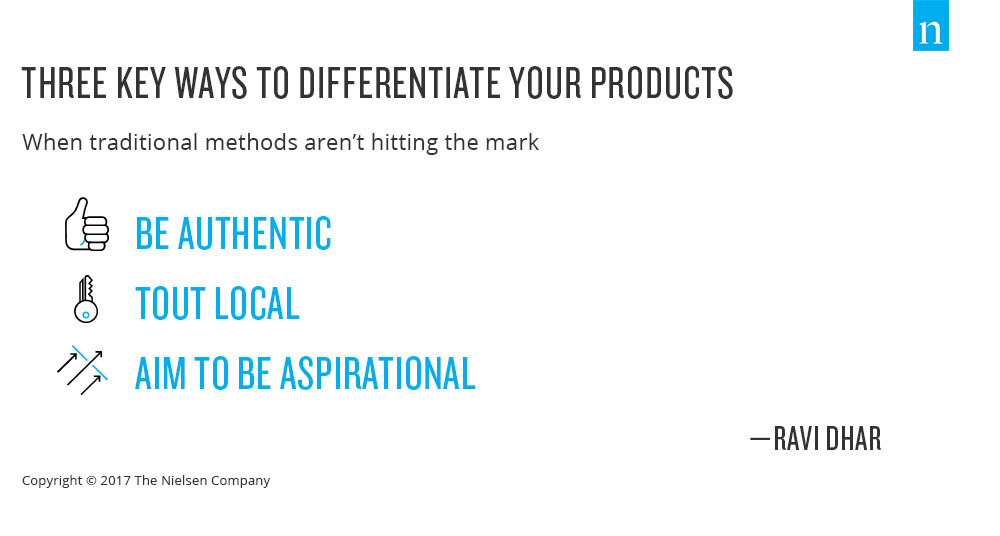

Before diving into the discussion, Dhar called out three themes that he said are helping companies succeed when traditional strategies aren’t hitting the mark:

- Authenticity: Consumers are gravitating toward messages that convey truth and credibility.

- Local: Much like patronizing socially responsible brands, consumers are drawn to companies that champion their local roots.

- Aspirational messaging: Brands with a drive to achieve something bigger—something beyond dollars on a balance sheet—are attractive to evolving consumers.

In looking at the recipe for change at Ainsworth Pet Nutrition over the past few years, it’s clear that each of the elements Dhar outlined have played a role in what has been nothing short of a significant transformation. Ainsworth, an 85-year-old company, made a conscious decision 10 years ago that its long-maintained strategy to be a regional, entry-price pet brand wasn’t the best way forward. Rather, the company observed Americans’ willingness to trade up in the pet category and decided to pivot to become a super-premium player to capitalize on the growth. And much of that has come via the company’s partnership with Rachel Ray and the Nutrish brand.

“It’s been a real change journey, said Jeff Watters, president and CEO. “We had an understanding about human adjacency trends and trading up, and we didn’t think premiumization should be limited to elite or exclusive. So we created a solution that meets the needs of all American pet families.”

The story at the Craft Brew Alliance (CBA) is similar, as the evolution of consumer preference has dramatically shifted the company’s focus in recent years. Specifically, Andy Thomas, CEO of CBA, explains that its Kona Brewing brand, which it acquired in 2010, now accounts for 55%-60% of the company’s revenue. Comparatively, revenue from its two founding brands, Red Hook and Widmer, is declining.

“With Kona, we just found that it’s a very relevant brand for people,” said Thomas. “The roots are tied to Hawaii—it’s liquid Aloha. It’s almost globally relevant to everyone.”

Unlike Ainsworth, Thomas stressed that in addition to tapping into something that resonates with consumers, CBA has made a conscious decision to not sell everywhere. Rather, the company has a very disciplined focus that centers on market appetite within specific markets—and then they double down there.

“We’ve really resisted the temptation to be everywhere,” he said. “We tried to determine where we wanted to win. When you’re our size, you can’t really compete if you try to be everywhere. But when you’re strategic, you can compete with the big guys—just on a more limited geographic scale.”

For both Ainsworth and CBA, a big component of their recent successes has been knowing when to migrate away from or de-prioritize legacy brands—brands that were foundational and responsible for getting the companies to where they are today. For Ainsworth, that meant deciding that a 75-year-old solution wasn’t the right one for the next 75 years.

“Migrating away from legacy brands has been an ongoing topic of conversation,” said Ainsworth’s Watters. “Our position with the board has been that the consumer and marketplace will tell us when the legacy brand outlives its usefulness. For us, the consumer voted with their wallets and told us that the heritage brands are the solution going forward.”

At CBA, the shift has centered on geographic positioning. Specifically, Thomas said CBA’s Red Hook and Widmer brands found themselves in markets where they couldn’t compete because they’re not known nationally. But rather than shutter them completely, CBA has made a conscious effort to market them where they can compete—in the markets they were born in.

“When it comes to lessons learned, listen to what the brands are telling you,” Thomas said. “Check your ego at the door and listen to the brands. The other big factor is culture and work environment—and embed that culture throughout your entire organization.”